In this series, we’re using cutting-edge AI research tools, including an unreleased deep research tool to look at the desktop 3D printing filament market. We’re then comparing it with our known data to see where AI research tools make sense, and where (and how) they make mistakes. The idea is to at the same time let your learn about the current state of the desktop 3D printing filament market, while also honing your AI skill and knowing if you should be using LLMs for research at all.

Here, (as we can see from the image above) the LLM was a bit feckless with the data. If we look at more sources, especially European ones, then Recreus has a strong position in high-quality flexible materials. But the scraping tool missed the European vendor entirely. Also, TPU is widely sold; it’s just that no one excels in it. Online mentions, forum mentions, and things like this skewed the overall perception towards Ninja as well. I’m not saying it’s bad; it’s good stuff, but for many things, Recreus is much better, especially for footwear. Of late, Recreus has also been much more innovative. But, there are more novices talking about getting TPU to work in the US than there are talking in-depth about footwear TPU publicly. The scraping tool also did not at all find ColorFabb’s Varioshore TPU. This is probably the single biggest innovation in TPU. In orthotics and beyond, it’s Varioshore that is doing incredibly well because you can program it. Perhaps because people call it Varioshore it hadn’t seen it as TPU? Because the scraping tool missed ColorFabb TPU and Recreus, it spotted this huge market gap in TPU. I left this in there to illustrate a point. Check, check, check again. Because it’s so easy to screw this up. Imagine a company new to filament looking at this and concluding that the TPU market is wide open because the tool essentially missed two of the major competitors.

I completely don’t agree that PEEK and TPU are similar. TPU, for many people, would be much more price-sensitive. If I’m doing something with PEEK, it’s because I need to use PEEK, which means that this expensive application or part is critical somehow, and I may be able to and want to pay for quality. For TPU, this is less of an issue, and things that need to work, such as shoes or braces, are high-volume items, so I’d want much better pricing and be sensitive to it. So again, the slide looks great initially but is super misleading. And indeed, if this were a cornerstone to planning your market entry, you would make the wrong decision.

PEEK is complex, and the tolerances, equipment, and material cost are high. Also, for some reason, Notebook kept throwing in BASF in the Engineering tier because of Ultrafuse. This could also be confusing.

Churn & Premium Buying (And Blatant AI Errors)

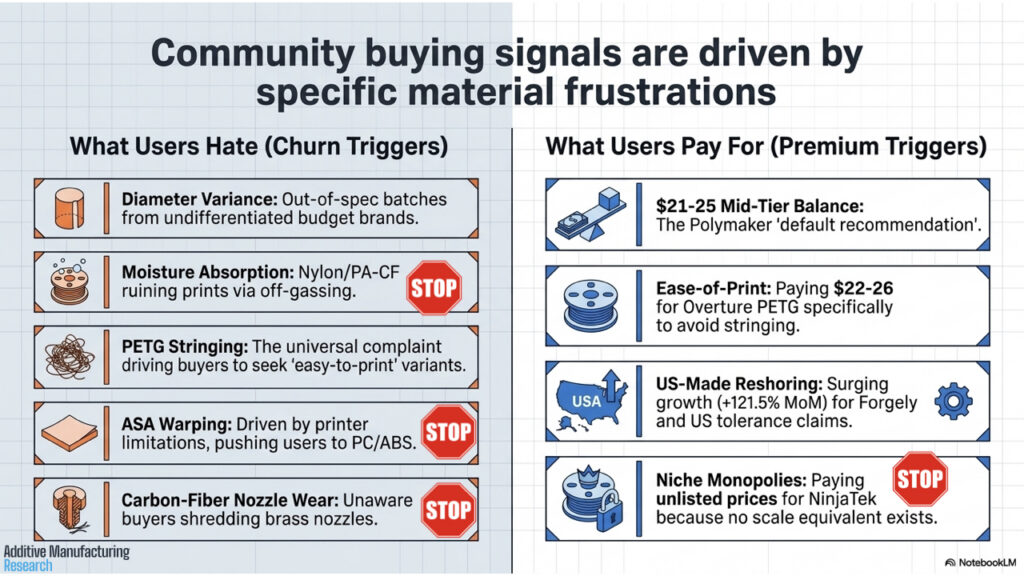

Now, the above chart is very pretty; it’s also very wrong. Off-gassing is not what ruins prints; it’s outgassing. Moisture absorption itself causes hygroscopic filaments to print badly, making breakage more likely, adhesion poor, and the material brittle as well. It’s the water itself that is being heated, escaping in steam, that causes bubbles, poor interlayer adhesion, and voids. The term the model wants to use here is outgassing (or steam expansion or hydrolysis), which refers to water escaping due to heat from the nozzle. Chemical off-gassing occurs when trapped VOCs and other chemicals are released at room temperature. Off-gassing is a risk to users, perhaps, or a risk when the finished part could release material over time, which could be important in a spacecraft, for example. Notebook conflated two data points and enmeshed them here. Again I’m not trying to be nitpicky here, but if you read the sentence literally from the slide, then you’ll get it wrong completely.

The ASA warping thing also looks plausible but is incorrect. PC ABS was already well known via Stratasys for many years. ABS was the very first filament used with desktop 3D printers and has always had warp issues. Better heated chambers and process control have reduced warp issues however for most users- For much of the market ASA is a newer, much rarer choice, and is growing. In particular, people are using ASA because it is excellent for outdoor use, and people have been making lots more outdoor things of late. So this point is completely incorrect. ASA warping specifically will not cause churn to other ASAs or other vendors; it will just cause people who use open printers to go back to PETG or PLA. Cheap closed printers will increasingly print the material well. I have no issues with ASA on the five different systems that I have at my home. And ABS warping, and warping in general in large parts, is a much bigger issue for people than ASA warping. I’m still pitching ASA to so many people as a material, and it’s not used as widely as it should be, and having it be summarized here as a major reason for people to switch between vendors is silly. Meanwhile, if we look at people who do want tougher or stronger materials, they’re looking towards polycarbonate. But new polycarbonate blends such as Prusament´s PC are not mixed with ABS, but with other additives and materials. So the point here is super misleading, especially since it is presented here as one of the major causes of churn.

The carbon fiber nozzle wear thing was relevant in the Ultimaker 2 days. Amazing point in 2011, less so now. This was a huge issue previously, but now, with stainless steel nozzles (and a strong aftermarket), it is no longer an issue. Yet, any online LLM today still sees this as a problem. I keep trying to delete this from the dataset. Of course there is a preference for steel nozzles now, (just look at the recent INDX kerfuffle) but apart from extremely abrasive materials this is a solved issue for the vast majority of users. Again, on the other hand, it says that, “no scale equivalent ” exists for Ninjatek, which is completely incorrect. ColorFabb and Recreus exist and are more innovative. The dangerous thing here is not that the AI makes mistakes, but that it masks them so well and makes them so plausible.

The Magic Slide

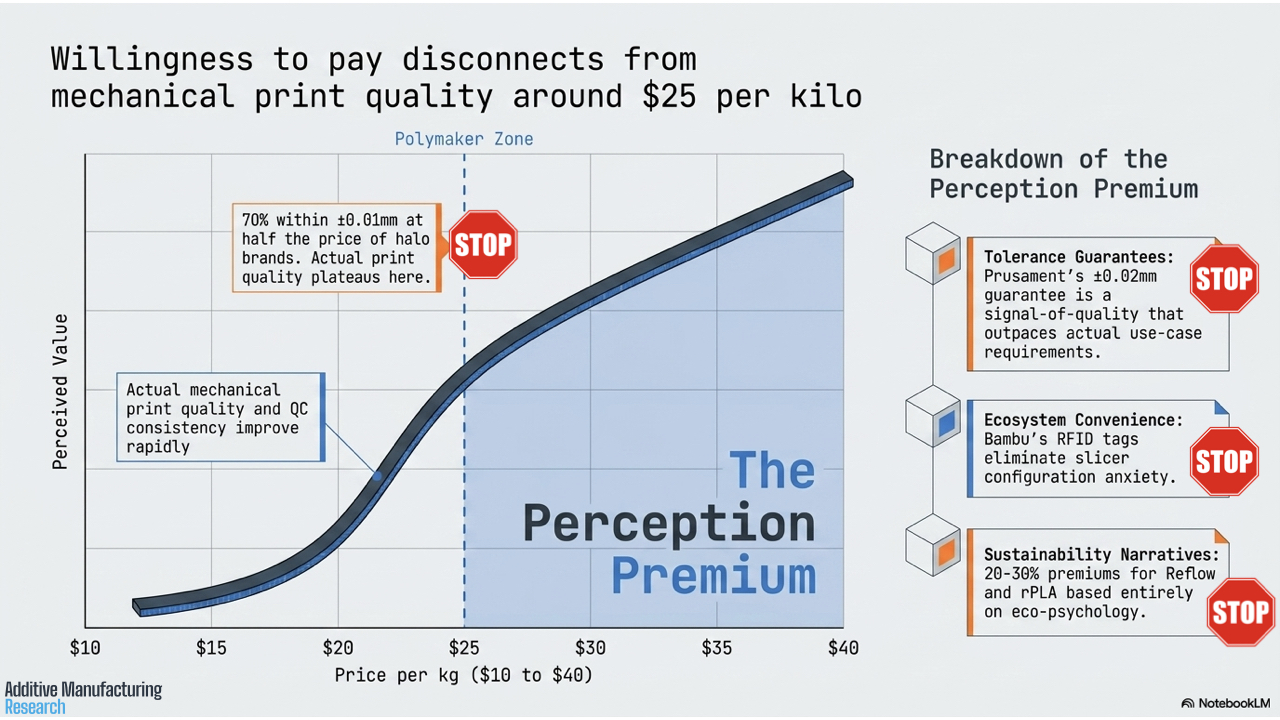

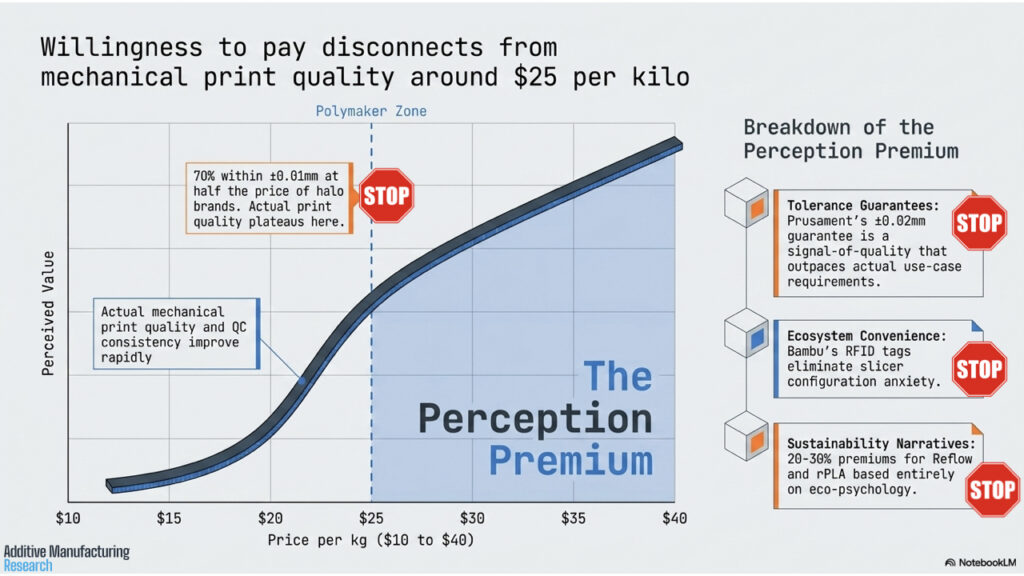

Now, when using AI as a research tool, we have these completely serendipitous moments that make it seem like you’ve gone and replicated an office full of McKinseyites all by your lonesome. Here is something I think would be interesting to discuss at a meeting. But it is false clarity. First off, the most important thing is that ovality really matters in filament. I could have a very tight tolerance for the filament dimensions, but if it is not the right ovality, I’ll still have big issues with it fitting well through the Bowden tube. Furthermore, when and where you measure really matters too. If I measure my filament once and the tolerance is good, it could still be all over the place for the rest of the filament. This will mean that more or less material is in the heat zone at more or less pressure throughout your build, wreaking havoc on everything. So the tolerance matters, but it should ideally be measured all along the entire filament, or at least many times. So this slide, which seems to give a lot of clarity, actually obfuscates the real issue. If you want to buy or make quality filament with tight tolerances all along the filament, continual ovality measurements matter. It’s not about a filament being a particular diameter, but about consistent extrusion.

I like that sustainability narratives come to the fore here, but Reflow is actually bankrupt. And I’ve never heard anyone say that they were anxious about slicer configurations; it was just annoying at the worst of times. If anything, new users tended to stick to the filament they knew previously because it was difficult for them to dial in new filaments. Now, people are freer to experiment. What the research tool completely missed was that many brands are now better at loading settings for various filaments. Printing on the whole is more stable now, and filament has improved, which makes printing easier. I do agree with the convenience factor, but there is a lot more going on than just the RFID tags.

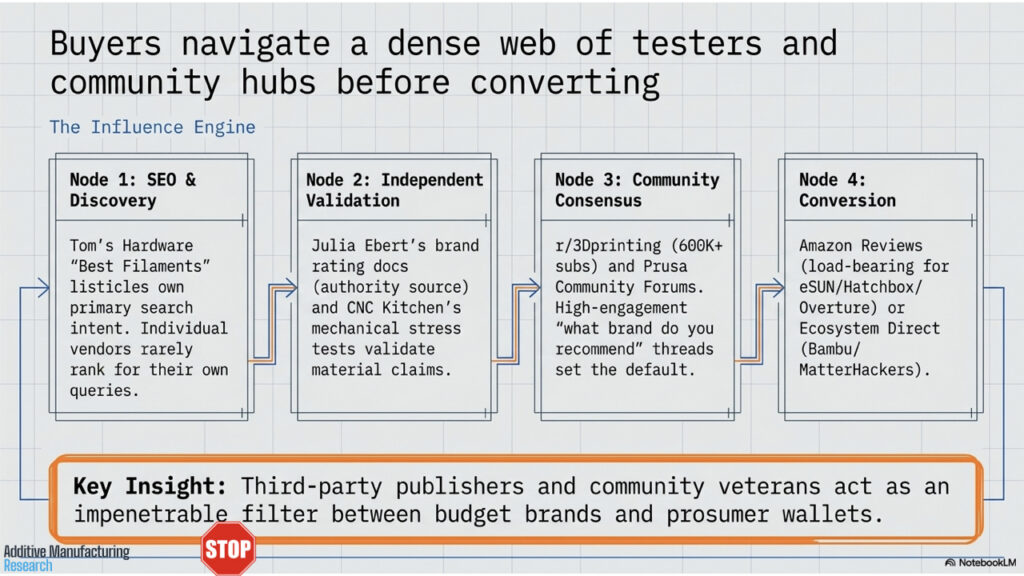

Buying Journey

I like this summation of many buying journeys, abandoned baskets, and more. We can see in 3D printing that community members on forums have been driving traffic and choice in filament brands for many years now. One thing underrepresented here is YouTube. YouTubers, through sponsorships, use in projects, and reviews, are driving a lot of buying now. Some of this is paired with kickbacks in the form of affiliate fees. Indeed, some YouTubers are making over $250,000 a year, mainly from 3D printer OEMs. So for the first time, a lot of the previously free, informed opinion is paid for. I know several of these people, and they generally seem upstanding and have real joy in their work. But the decision funnel will radically change over the coming years due to YouTube and affiliate. Before, if you canvassed opinion, it was from people who had no skin in the game. Everyone was giving their best advice based on their own experiences; now, with opinions flooded by commerce, we need to find new paths. We also don’t really have many filament testing and evaluation initiatives. There will be real scope and need for this. If we look at advertising and paid search, we can only assume that a lot of money is migrating directly to social as well, so this need will become more pressing.

I really don’t like the AI´s use of “impenetrable filter” here. First off, an impenetrable filter is not a filter. And this is yet another sign of the AI trying to be snazzy but hiding meaning, rather than bringing it to the fore. There are a series of filters that all inform opinion, but many people just buy the cheapest stuff available to them or try out a lot of things as well. So the wording here makes it seem like publishers own this space, and this is not the case. We saw this very clearly with the rise of the Amazon filaments that were initially not pushed at all by social media or users, but simply came up during Amazon searches by people who bought printers or dogfood there. Amazon completely replaced this channel. Many scarcely believed how big Hatchbox got because no one was mentioning it anywhere, but it was doing tens of thousands of spools. So again, the wording is seriously misleading here. If you read the slide alone, you’ll conclude that social media is the way to go. But, there are other distribution paths and paths to credence.

Conclusion

So how to conclude this part of the series? AI tools can be very powerful, but we must not forget that a lot of these tools have been made to be rather sycophantic. Here we’ve used some very powerful tools, and the results at first glance look amazing. Now, some of them are. I’m very pleased with the pricing information. I was very pleased to be able to index all the relevant forum discussions, comments, product pages, OEM pages, and pricing information. I was very pleased with the pricing trends and materials trends. But, there were a lot of inaccuracies. The most powerful finding (no one makes TPU!) was completely incorrect. Bankrupt companies were included. Old worries from years ago were touted as current problems. Snazzy summations gave people completely wrong ideas about the data. And some of the synthesized data was handled incorrectly. A nice slide would hold a lie. A summation of the major churn drivers was riddled with errors. The segmentation was good, the pricing data was good, and the low-volume amortization insight was good. But if you did not know the industry, the strategic choices that you’d take from this data would be incorrect. And I’m sure that if I had left these slides up without STOP signs all over, they would have ended up all over, giving the wrong impression.

So AI crawlers, indexing tools, LLMs, and research tools are powerful but misleading. Imagine having a bright erudite intern who drinks heavily during the day and occasionally does coke. That, to me, is the state of AI-aided research today. Fast and seemingly convincing, the words tumble out and seem to make sense until you stop and think. So be careful out there, folks. I think that AI-aided research is powerful stuff, but then again, so is coke. Eventually, this is going to be useful, but not before it ends a lot of careers.